Our website uses cookies

Our website uses cookies. By continuing, we assume your permission to deploy cookies as detailed in our Privacy Policy.

The credit union does not represent either the third party or the member if the two enter into a transaction.

Navigating your credit can sometimes feel like running through a maze with a blindfold on. From arbitrary numbers influencing your finances to reports, scores, and so many terms you don’t know. It’s hard to keep up.

In this guide, our EdiFi Experts have compiled a practical credit crash course to help you understand and conquer your credit. Whether you’re looking for a credit refresher or you’re jumping into the world of credit for the first time, get ready for some top-notch financial wisdom.

The textbook definition of credit is the ability to obtain goods or services before making a payment based on the trust that you’ll pay it back later. Essentially, credit is your financial reputation— the better your reputation, the more likely people are to trust you. The more likely people are to trust you, the more money they’ll let you borrow.

Credit comes in two different forms: Secured and unsecured.

Secured credit is backed by collateral, like property or assets, such as your car or your house. You can borrow larger amounts of money at lower interest rates. But if you don’t pay your secured credit back, the lender can take ownership of your collateral.

Unsecured credit relies solely on your credit— no collateral necessary. You may have to borrow less at a higher rate, but you don’t have to worry about losing any property or assets. However, if you don’t pay back your unsecured debt, you’ll go to collections, which can have serious consequences for your credit and financial future.

Have you ever looked at your credit report? If you haven’t, that’s okay! You use your credit report when you make certain, usually big, transactions, like applying for a mortgage or auto loan.

Your credit report is home to all your credit-related activity, like a financial report card that you carry with you from kindergarten through the rest of your life. Just like an academic report card, your credit report includes everything from personal information— like your name, address, and SSN —to the terms of your credit and credit history, such as your payment history, any tax liens on your property, and bankruptcy filings.

If your credit report is your financial report card, your credit score is like a student ID number. Your credit score is a 3-digit number that potential lenders use to calculate the likelihood of you repaying your debt.

Confused? Here’s the big-picture difference:

The most common type of credit score is a FICO score. FICO scores range from 300 to 850— the higher the better. EdiFi Experts consider anything above 670 to be good credit, and anything above 800 to be exceptional.

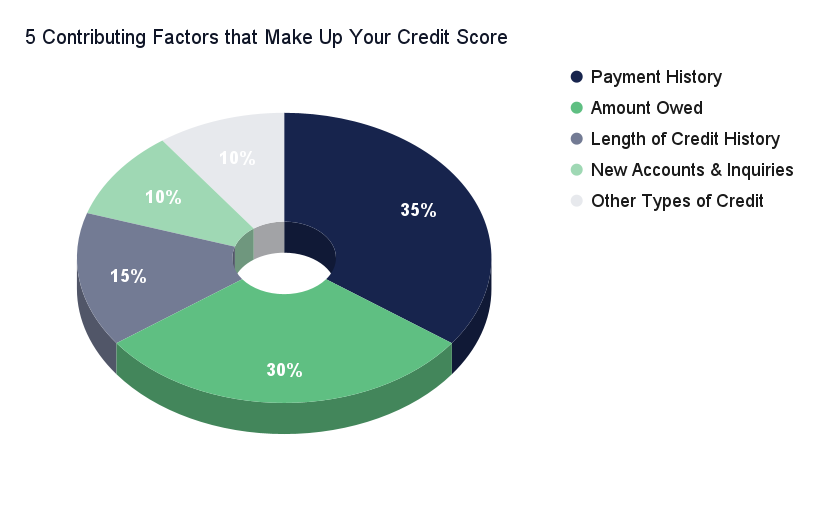

Reporters calculate your credit using five factors, each contributing a different percentage to your overall score. These factors are:

REMEMBER: Since Payment History and Length of Credit comprise half of your credit score, it’s vital you never close old credit cards! It doesn’t matter if you opened them when you were 18 and never use them anymore. Those credit cards are helping your credit score more than you know!

Since your credit score is so important, there are several ways to check it.

The Three Credit Bureaus: You can check your score and even access your report through Experian, Equifax, and TransUnion. Each credit bureau allows you to sign up for a free account and lets you freeze and unfreeze your credit, which essentially blocks anyone from accessing your score or report.

EdiFi’s KeepSafe Checking Account: With an EdiFi KeepSafe Checking Account, you can view a credit snapshot from the palm of your hand! Visit idprotectme247.com or access the Club Checking Mobile App to access your benefits. You can download the Club Checking Mobile App on the App Store or Google Play Store.

FreeCreditReport.com: This website lets you access your credit report from each bureau for free once a year. That means three free credit reports per year! Our EdiFi Experts suggest checking one bureau per quarter.

Credit Karma: Chances are, you’ve heard about Credit Karma’s unlimited, free access to your credit score— and it’s true, they’re a good credit resource! However, Credit Karma makes money from selling credit-building services, and as a result, it will report your score lower than other credit reporters. If you use them, be sure to double-check your credit with another resource.

Credit is crucial to your financial success, and while it seems confusing, it doesn’t have to be! Our Financial Experts are here to answer your questions and help you know more and grow more.

In our next credit article, we’ll discuss why it’s important to have good credit and how to improve your credit score!

.jpg)